I hear the first sentence from my clients all the time and I often reply with the second. Trusts are a tremendous asset and something that can protect ourselves and our loved ones, but it comes with caveats. What many people do not understand is that there is no one-size-fits-all option. This is because we all have our own unique needs, especially when it comes to estate and long-term care planning.

While some may not need a trust, others may need one for long-term care planning, tax planning, caring for an individual with special needs, or for protecting a child’s inheritance from creditors or even the child themselves.

It all depends on your specific needs at certain points in your life. More often than not, the “I’m all set, I have a trust,” reply is followed by a discussion on the differences between revocable and irrevocable trusts.

What To Know

The one we call Revocable, or as it’s also known as a living trust, is in which terms, gifts, and clauses can be changed at any time. An irrevocable trust is the opposite, in that it refers to one that cannot be modified after it has been created.

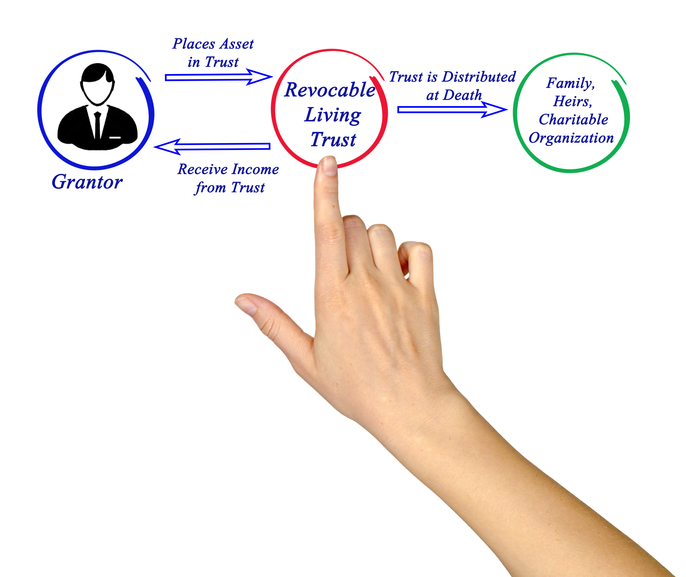

Let’s take one step back to describe what one is. It is a separate legal entity. These trusts are set up by a person to hold assets, referred to as a trustmaker, to manage assets. Trusts are up drawn up during the original maker’s lifetime to assure that assets are used in a way in which he or she deems appropriate. These assets are retitled within and managed by a party known as the trustee. The trustee manages those assets within the trust while the trustmaker is alive, incapacitated, and even after their death. Depending upon the language within, the trustee may be able to determine how the assets are invested and to whom they are distributed. When the trustmaker dies, the trustee must manage it in accordance with the guidelines laid out when the trust was formed.

Revocable Living Trust

The trustmaker of a revocable living trust may change its terms at any time. They may remove beneficiaries, designate new ones, and modify stipulations as to how assets within it are managed. Of course, these new designations must be completed before the trustmaker passes away. A trustee cannot make these changes.

Revocable living trusts have many advantages. First, any property that is owned by the trust passes outside the probate court which means that your beneficiaries can receive their inheritance quicker without any probate court involvement.

For anyone, who has had the duty to serve as an executor or personal representative of one’s estate, you know how cumbersome, costly, and time-consuming the probate process can be.

Secondly, a revocable trust maintains privacy which can be important to all parties involved. Lastly—and the most common reason for my young clients with families—it preserves assets for minor children until they reach any age you have selected.

The revocable living trust is what I normally recommend because as an estate-planning attorney, my job is to plan for the what-ifs. For example, what if something happens to Mom and Dad at the same time? Who will care for their children and how will their children’s assets be managed?

With a trust, parents can continue to dictate how their child’s inheritance will be managed, after their passing, through specific clauses embedded within it. For example, “Joey will receive 50% of his inheritance at age 25 and the other 50% at age 30.” Without a trust, Joey will be able to obtain 100% of his inheritance at age 18. Think back to when you were 18, can you imagine the poor decision making that would have occurred if you just inherited $500,000?

Given the above reasons and flexibility of revocable living trusts in contrast with the rigidity of an irrevocable trust, it seems all trusts should be revocable. However, there as some key disadvantages to a revocable living trust.

First, the trustmaker retains control over a revocable trust, which means the assets funded into the trust are not shielded from creditors the way they are considered irrevocable. If the trustmaker is sued, the court may order the trust assets to be liquidated to satisfy any judgment. Another disadvantage is that when the trustmaker dies, the assets held in trust are subject to both state and federal estate taxes.

Irrevocable Trust

The terms of an irrevocable trust, in contrast, are set in stone the minute that it is signed. Except under exceedingly rare circumstances, no changes may be made to an irrevocable one.

The trustmaker, having transferred their assets into the trust, effectively removes all rights of ownership to the assets and—for the most part—any control. The most common reasons for irrevocable trusts are for tax purposes and long-term care planning.

Irrevocable trusts remove the assets from your taxable estate, meaning they are not subject to an estate tax upon death. The second and most popular reason to establish an irrevocable trust is for long-term care planning. As with a revocable one, you create it during your lifetime. The key here is that you cannot maintain any sort of control of this trust, which means you cannot be the trustee and/or a beneficiary. The goal for this type is to protect assets funded within the trust from creditors, which may include a nursing home.

For more information on revocable living trusts and irrevocable trusts, please feel free to contact our office at jebacher@ebacherlaw.com and (978) 269-4485 as we are happy to assist you.